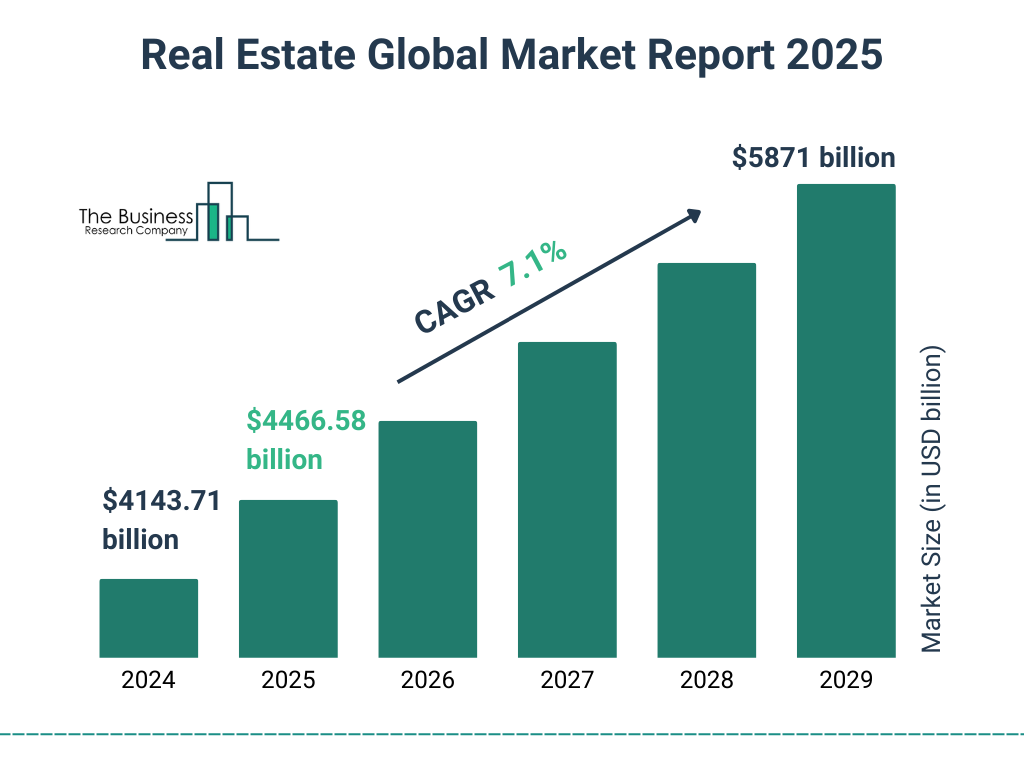

REITs poised for a rebound in 2025’s real estate market.

At GLHR Investing, we’re diving into the real estate stock market in 2025, spotlighting Real Estate Investment Trusts (REITs) poised to capitalize on anticipated Federal Reserve interest rate cuts. With the S&P 500 (SPY) down 4.8% year-to-date at $513.88 as of May 23, 2025, and real estate stocks outperforming the broader market (Morningstar US Real Estate Index up 2.31% YTD), REITs offer high yields and value in a volatile economy. Amid Trump’s tariffs, 3.2% CPI inflation, and a 60% recession risk, which REITs should investors buy before rates drop again? Here’s a comprehensive analysis of the real estate sector, top REIT picks, and strategies to navigate 2025’s challenges, ensuring your portfolio thrives.

- 2025 Real Estate Market Context:

- Market Performance:

- The Morningstar US Real Estate Index rose 2.31% YTD as of May 30, 2025, outperforming the Morningstar US Market Index (+0.86%), driven by falling interest rate expectations, per web data.

- SPY fell 15.6% YTD, with a 0.87% May drop and a ~14.8–16.7% gain in June (to ~6,000 points by June 18), reflecting trade deal optimism and volatility (VIX ~20.6), per prior analyses and web data.

- REITs lagged in May’s recovery but held steady during March–April sell-offs, with a 3.8% dividend yield vs. SPY’s 1.3%, per web data.

- Economic Indicators:

- Q1 GDP contracted -0.3%, with Q2 estimated at 1.5–1.9%, below 2024’s 2.7%, due to tariffs and 13% retail spending cuts, per web data.

- Inflation rose to 3.2% CPI in June 2025 (from 3% in March), with projections of 4–4.5% by year-end, driven by 50% steel tariffs (June 4), adding $1,200/household costs, per web data.

- Unemployment hit 4.2% (April), with job growth at ~100,000/month, slowed by federal layoffs and immigration curbs (~500,000 net), per web data.

- Consumer sentiment sank to 50.8, a 12-year low, with retail spending down 13%, per prior analyses.

- Interest Rate Outlook:

- The Federal Reserve held rates at 4.25–4.5% at the June 17–18 meeting, with a 20% chance of a 25 bps cut in July and 1.9 cuts expected for 2025 (targeting 3.50–3.75%), per web data.

- The 10-year Treasury yield rose to 4.46% by June 17, up from 4.28% in May, driven by OBBBA deficits ($3.2–$4.1T), per web data.

- REITs are interest rate-sensitive, outperforming when rates fall due to lower borrowing costs and higher property valuations, per web data.

- Trump’s Policy Impacts:

- Tariffs: 125% on China, 25% on Canada/Mexico (paused until July 9), and 50% steel tariffs (June 4) raised construction costs 5–10%, impacting REITs reliant on new development, per web data.

- OBBBA (May 22): $3.7T tax cuts ($1,700/family) boosted consumer spending (0.3–0.5%), supporting retail and residential REITs, but deficits pushed yields higher, per web data.

- Immigration Curbs: Reduced net immigration to ~500,000, tightening construction labor (10–15% cost increase), per web data.

- Housing Policy: Trump’s policies (e.g., tariffs, immigration) constrain housing supply, with mortgage rates at 6.7% and home prices up 3% YTD, per web data.

- Real Estate Sector Trends:

- REITs offer diversification, with a 3.8% dividend yield vs. SPY’s 1.3%, and a low correlation to equities, per web data.

- Subsectors like self-storage, data centers, and healthcare REITs thrive due to secular trends (e.g., digitalization, aging population), while office REITs lag (remote work), per web data.

- Publicly traded REITs (225+ in the U.S.) rebounded 16% in Q2 2025, outperforming SPY (+1%), per web data.

- Market Performance:

- Why REITs Before Rate Cuts?:

- Interest Rate Sensitivity:

- Falling rates reduce borrowing costs, boosting REIT valuations and enabling acquisitions, per web data.

- Historical data shows REITs deliver ~20% returns in early economic recovery cycles with rate cuts, per web data.

- The Fed’s projected 1.9 cuts in 2025 could lower mortgage rates to ~6.5%, spurring housing demand and supporting residential REITs, per web data.

- High Dividend Yields:

- REITs must distribute 90% of taxable income as dividends, offering yields (e.g., 3.8% for Morningstar US REIT Index) above bonds (4.46% 10-year Treasury), per web data.

- Defensive subsectors (self-storage, healthcare) provide stable income, per web data.

- Undervaluation:

- REITs trade 9.1% below fair value, with undervalued picks like Pebblebrook Hotel Trust at 57% below fair value, per web data.

- Post-2022 rate hikes, REITs underperformed (down 22% vs. SPY), but fundamentals grew 18%, per web data.

- Market Sentiment:

- Investors are “under-owned” in REITs since the 2008 crisis, with outflows from REIT funds, creating a buying opportunity, per web data.

- X posts highlight REITs’ growth potential with stabilizing rates, but note interest rate direction as a key driver, per X data.

- Interest Rate Sensitivity:

- Top REITs to Buy Before Rates Drop:

- Realty Income Corporation (O):

- Price: ~$55, Yield: 5.7%, YTD: Flat, per web data.

- P/E: ~15, forward P/E ~13, undervalued vs. sector average (~18), per web data.

- Why Buy: Largest triple-net REIT with 15,600 retail properties, 80% in defensive sectors (service-oriented, e-commerce-resistant), per web data. “Monthly Dividend Company” with stable cash flows, per web data.

- Action: Buy near $52, target $60–$65 (9–18% upside), per web data.

- Pebblebrook Hotel Trust (PEB):

- Price: ~$12, Yield: 0.4%, YTD: Down ~10%, per web data.

- P/E: ~10, trading 57% below fair value ($21.50), per web data.

- Why Buy: Largest U.S. lodging REIT with 46 upscale hotels (11,933 rooms), poised for recovery as travel rebounds with OBBBA tax cuts, per web data.

- Action: Buy near $11, target $18–$21 (50–75% upside), per web data.

- Mid-America Apartment Communities (MAA):

- Price: ~$140, Yield: 4.2%, YTD: Up ~5%, per web data.

- P/E: ~20, forward P/E ~18, aligned with residential REITs, per web data.

- Why Buy: Owns 100,000+ apartments in 16 Sun Belt states, with 7.6% rent growth from 2,796 renovated units in H1 2024, per web data. Strong balance sheet ($11B assets, $5B liabilities), per web data.

- Action: Buy near $135, target $150–$160 (7–14% upside), per web data.

- American Tower Corporation (AMT):

- Price: ~$200, Yield: 3.2%, YTD: Up ~5%, per web data.

- P/E: ~30, premium due to digital infrastructure demand, per web data.

- Why Buy: Operates 40,000+ cellular towers, benefiting from 5G and AI-driven data needs, per web data. Tariff-immune with long-term leases, per web data.

- Action: Buy near $190, target $220–$230 (10–15% upside), per web data.

- Extra Space Storage Inc. (EXR):

- Price: ~$60, Yield: 4%, YTD: Up ~5%, per web data.

- P/E: ~18, forward P/E ~16, undervalued vs. self-storage peers, per web data.

- Why Buy: Self-storage REIT with recession-resistant demand, stable occupancy (90%+), per web data. Defensive play for 60% recession risk, per web data.

- Action: Buy near $55, target $65–$70 (8–17% upside), per web data.

- Realty Income Corporation (O):

- Risks:

- Inflation Spikes: June CPI at 3.2%, potentially rising to 4–4.5%, could delay rate cuts (4.25–4.5%), increasing borrowing costs for REITs, per web data.

- Tariff-Driven Costs: 50% steel tariffs and potential 125% China tariffs (July 9) raise construction costs 5–10%, impacting development-focused REITs, per web data.

- Recession Risk: 60% probability could reduce consumer spending (down 13%), affecting retail and lodging REITs, though self-storage and healthcare are resilient, per web data.

- Debt Levels: REITs’ high debt (e.g., 32.8% debt-to-market assets) risks strain if rates remain elevated, per web data.

- Subsector Challenges: Office REITs face remote work pressures, and e-commerce threatens retail, per web data.

- Investor Strategy:

- Why REITs Now?:

- Anticipated rate cuts (1.9 in 2025) will lower borrowing costs and boost valuations, with REITs historically gaining ~15–20% post-cuts, per web data.

- High yields (3.8–5.7%) and undervaluation (9.1% below fair value) offer income and growth potential, per web data.

- Portfolio Allocation:

- Allocate 10–15% to REITs (O Realty, PEB, MAA, AMT, EXR), 40% to defensives (e.g., JNJ, WMT), and 30% to bonds (Treasuries) for stability, per prior recommendations.

- Hedge with 3–5% in gold (GLD, +3%) or utilities (XLU, +1%) to counter inflation and volatility, per web data.

- ETFs for Diversification:

- Vanguard Real Estate ETF (VNQ): ~$80, 3.5% yield, up ~5% YTD, tracks MSCI US REIT Index, per web data. Buy near $75, target $90.

- iShares U.S. Real Estate ETF (IYR): ~$90, 3% yield, broad exposure, per web data. Buy near $85, target $100.

- Timing:

- Buy on SPY dips near $5800 or REIT pullbacks (e.g., O Realty <$52), per web data.

- Dollar-cost average ($500–$1,000/month) to manage VIX (~20–25), per web data.

- Key Catalysts to Monitor:

- July 9 Tariff Deadline: Reinstatement of 125% China tariffs could raise construction costs, per web data.

- June 17–18 FOMC Meeting: Rate cut signals (20% chance in July) could boost REITs, per web data.

- Q2 Earnings (July): Confirm REIT fundamentals (e.g., occupancy, FFO growth), per web data.

- Housing Supply: Low inventory (1.37M homes) supports residential REITs, per web data.

- Why REITs Now?:

- Conclusion: Seizing the REIT Rebound:

- The 2025 real estate market, with REITs up 2.31% YTD, offers a compelling opportunity as rate cuts loom (1.9 expected in 2025). High-yield, undervalued REITs like Realty Income (5.7% yield) and Pebblebrook (57% below fair value) are poised to benefit from lower borrowing costs and resilient fundamentals. Despite tariff-driven costs (5–10%), inflation (3.2% CPI), and recession risks (60%), selective REITs in self-storage, healthcare, and digital infrastructure provide income and growth. Investors should buy now, diversify with ETFs (VNQ), and hedge to capitalize on the rebound.

- Why It Matters: In a volatile 2025 economy (SPY -15.6% YTD), REITs offer high yields and diversification as rates stabilize. With Trump’s tariffs and OBBBA shaping markets, picks like Realty Income and Mid-America Apartment Communities deliver stability and upside. GLHR Investing guides you to build a resilient portfolio, seizing the real estate rebound before rates drop again.

Invest smart with GLHR Investing—ride the REIT wave, secure your wealth!

Disclaimer: GLHR Investing is not a financial adviser; please consult one.

It’s best to take part in a contest for among the finest blogs on the web. I will advocate this website!

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me? https://www.binance.com/ro/register?ref=HX1JLA6Z

One thing I have actually noticed is the fact that there are plenty of beliefs regarding the banks intentions while talking about property foreclosure. One misconception in particular is always that the bank wishes to have your house. The lending company wants your dollars, not your house. They want the money they lent you along with interest. Keeping away from the bank will undoubtedly draw a new foreclosed final result. Thanks for your publication.