Fed rate cuts could ignite small-cap stocks in 2025.

At GLHR Investing, we’re zooming in on the U.S. Federal Reserve’s interest rate policy in 2025, a pivotal factor shaping the $1.7 trillion small-cap stock market. With the S&P 500 (SPY) at $513.88, down 4.8% year-to-date as of May 23, 2025, and the Fed holding rates at 4.25–4.5%, investors are eyeing potential rate cuts to spark a small-cap rally. Amid Trump’s tariffs, 3% inflation, and a 60% recession risk, could the Fed’s next move ignite small-cap stocks like those in the Russell 2000? Here’s a comprehensive analysis of U.S. rates, Fed policy expectations, Trump’s influence, and how rate cuts could fuel small-cap opportunities, with strategies for investors in a volatile economy.

- U.S. Interest Rates in 2025: Current Landscape:

- Federal Funds Rate:

- The Fed maintained rates at 4.25–4.5% through its May 2025 meeting, following a 1% cut in H2 2024 (from 5.25–5.5%), per web data.

- This range, unchanged since December 2024, reflects resilient economic data (2.6% Core PCE inflation in March) and tariff-driven inflation risks, per web data.

- Treasury Yields:

- The 10-year Treasury yield rose to 4.28% by June 2025 (from 4.40% in late 2024), driven by Trump’s “One, Big, Beautiful Bill” (OBBBA) deficit concerns ($3.2–$4.1T) and tariff-induced inflation expectations, per prior analyses.

- The 2-year yield, tracking Fed expectations, climbed to 4.35% from 4.25% in December 2024, signaling reduced cut expectations, per web data.

- Inflation Dynamics:

- Inflation held at 3% through March, rising to 3.5–4% by June due to 50% steel tariffs (June 4) and import cost hikes ($1,200/household), per prior analyses.

- Core PCE, the Fed’s preferred gauge, was 2.5% in April, down from 2.6% in March, but tariff risks could push it to 2.8% by year-end, per web data.

- Economic Context:

- Q1 2025 GDP contracted by -0.3%, with Q2 estimated at 1.5–1.9%, below 2024’s 2.7%, due to tariff disruptions and spending cuts (13%), per prior analyses.

- Unemployment rose to 4.2% by April, with job growth slowing to ~100,000/month, reflecting federal layoffs and immigration curbs (~500,000 net), per web data.

- Consumer sentiment hit a 12-year low (50.8), with retail spending down 13%, per prior analyses.

- Federal Funds Rate:

- Federal Reserve’s Policy Outlook: The Next Move:

- Current Stance:

- The Fed held rates steady at its June 17–18 meeting, citing “resilient economic data” and tariff-driven risks of “rising unemployment and prices,” per web data.

- Chair Jerome Powell emphasized patience, noting a “solid” economy but risks from Trump’s policies, per web data.

- Rate Cut Expectations:

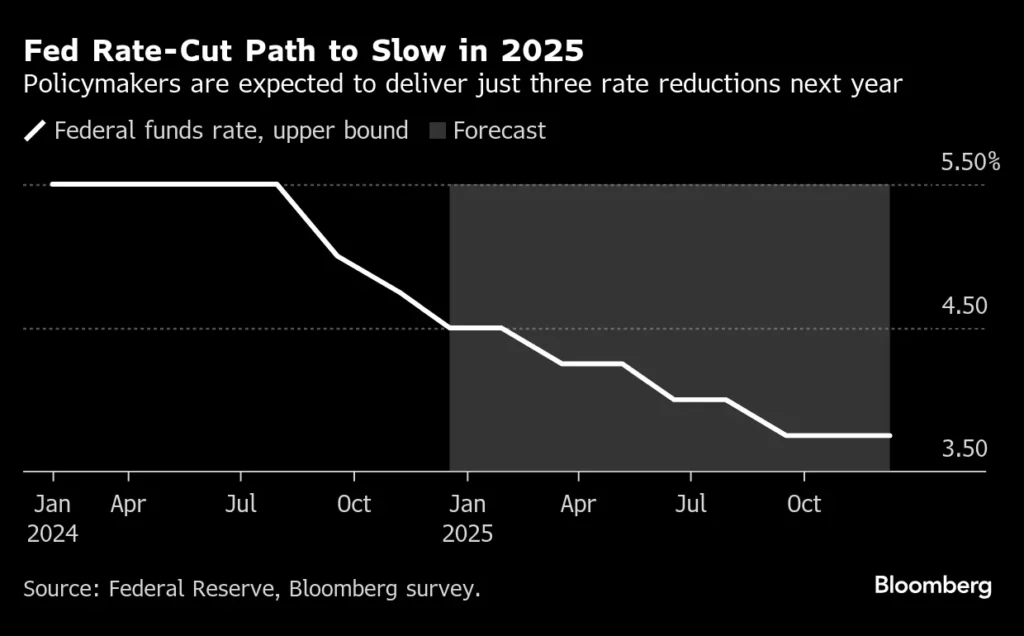

- Investors anticipate 1–3 cuts in H2 2025, targeting 3.50–3.75% by year-end, with September 17 as a likely start (25 bps), per X post (@grok).

- Fed projections (March 2025) indicate two cuts (0.5% total) for 2025, down from four expected in September 2024, due to sticky inflation (2.8% core PCE forecast), per web data.

- Markets price in ~33 bps of cuts for 2025, down from 49 bps post-December 2024, reflecting a hawkish shift, per web data.

- Influencing Factors:

- Inflation Risks: Tariffs (125% China, paused until July 9) and steel tariffs (50%) could push inflation to 4–4.5%, limiting cuts, per web data.

- Economic Slowdown: -0.3% Q1 GDP and 4.2% unemployment signal recession risks (60%), potentially forcing cuts if growth falters, per web data.

- Trump’s Pressure: Trump’s May 2–7 Fed criticism demanded cuts, but Powell’s independence held firm, per prior analyses. Tariff policies (e.g., May 23 Apple threat) add uncertainty, per web data.

- Market Sentiment:

- X posts (@charliebilello, @grok) suggest a cautious market, expecting steady rates in June/July but cuts by September if inflation eases or tariffs soften, per X posts.

- The VIX (~20.6 in June) and Fear & Greed Index (~45, neutral) reflect uncertainty, with investors hedging via gold (GLD, +3%), per prior analyses.

- Current Stance:

- Trump’s Policy Influence on Rates and Small-Caps:

- Positive Impacts:

- OBBBA Tax Cuts (May 22): $1,700/family savings and corporate relief (100% expensing) could boost small-cap spending and earnings (42% growth forecast for 2025), supporting firms like LCI Industries (LCII), per web data.

- Reshoring Policies: CHIPS Act and Infrastructure Investment and Jobs Act drive domestic investment, benefiting small-cap industrials (e.g., Brunswick, BC), per web data.

- Deregulation: Trump’s pro-growth agenda (e.g., reduced AI oversight) could lower small-cap compliance costs, per prior analyses.

- Negative Impacts:

- Tariffs (April–June): 125% China tariffs (paused July 9) and 50% steel tariffs (June 4) raise input costs 10–20%, squeezing small-cap margins, per web data.

- Deficit Concerns: OBBBA’s $3.2–$4.1T deficit pushed yields (10-year at 4.28%), reducing rate cut odds and pressuring small-cap valuations, per web data.

- Immigration Curbs: Reduced labor supply (~500,000 net immigration) increases small-cap labor costs, particularly in consumer services, per prior analyses.

- Market Reaction:

- Tariffs triggered SPY drops (12.1% intra-month April, 0.5–1% June 1–6), with small-caps (Russell 2000, -4.4% on December 18, 2024) hit harder due to debt sensitivity, per web data.

- OBBBA optimism lifted consumer services (e.g., TJX, +0.5% June 3–4), but deficit fears capped gains, per prior analyses.

- Positive Impacts:

- How Rate Cuts Could Ignite Small-Cap Stocks:

- Why Small-Caps Benefit:

- Debt Sensitivity: Small-caps hold more floating-rate debt than large-caps, making rate cuts (e.g., 25 bps) a direct earnings boost by lowering interest expenses, per web data.

- Earnings Growth: Analysts forecast 42% earnings growth for Russell 2000 in 2025 (vs. 6% in 2024), outpacing large-caps (14.5%), per web data.

- Valuation Appeal: Small-caps trade at a discount (P/E ~15 vs. S&P 500’s ~22), offering value if cuts spur growth, per web data.

- M&A Activity: Lower rates reduce capital costs, boosting M&A (e.g., small-cap biotech), with large-caps holding record cash, per web data.

- Historical Context:

- Small-caps outperformed large-caps in past rate-cut cycles (e.g., 1995, 2001) when no recession followed, with Russell 2000 gaining ~20% in 12 months post-first cut, per web data.

- In 2024, Russell 2000 rose 9% in July amid cut expectations, outpacing SPY’s 2.5%, per web data.

- Challenges:

- Tariff Headwinds: 10–20% cost increases from tariffs could offset rate cut benefits for small-caps in consumer durables (e.g., LCII), per web data.

- Recession Risk: A 60% recession probability could dampen demand, with small-caps’ weaker balance sheets more vulnerable, per web data.

- Fewer Cuts Expected: The Fed’s hawkish shift (two cuts vs. four) and rising yields limit small-cap upside, with Russell 2000 tumbling 4.4% on December 18, 2024, per web data.

- Market Performance:

- Russell 2000 fell ~1–1.5% in June’s first week (June 1–6), with SPY down 0.5–1%, reflecting tariff fears over cut hopes, per prior analyses.

- Small-caps gained 10% in July 2024 on rate cut optimism but lagged YTD (-19% vs. SPY’s -15.6%), per web data.

- Why Small-Caps Benefit:

- Top Small-Cap Stocks to Watch:

- LCI Industries (LCII):

- Price: ~$110, Yield: 3.8%, YTD: Flat, per web data.

- Why Notable: RV and marine parts supplier, benefits from consumer spending if cuts boost demand, per web data.

- Outlook: Undervalued (P/E ~15), buy on dips near $100 for ~20% upside by 2026, per web data.

- Brunswick Corporation (BC):

- Price: ~$80, Yield: 2.0%, YTD: Down 5%, per web data.

- Why Notable: Marine recreation products, poised for discretionary spending revival, per web data.

- Outlook: P/E ~12, buy near $75 for $90–$100 target, per web data.

- Winmark Corporation (WINA):

- Price: ~$400, Yield: 0.9%, YTD: Up 10%, per web data.

- Why Notable: Resale retail (Plato’s Closet), recession-resistant, per web data.

- Outlook: P/E ~20, buy on dips near $380 for ~15% upside, per web data.

- Verra Mobility Corporation (VRRM):

- Price: ~$30, Yield: 0%, YTD: Up 15%, per web data.

- Why Notable: Traffic tech solutions, stable cash flows, per web data.

- Outlook: P/E ~18, buy near $28 for $35 target, per web data.

- Insight Enterprises, Inc. (NSIT):

- Price: ~$200, Yield: 0%, YTD: Up 12%, per web data.

- Why Notable: IT solutions, benefits from AI data center spend, per web data.

- Outlook: P/E ~15, buy near $190 for $220–$230 target, per web data.

- LCI Industries (LCII):

- Investor Strategy:

- Rate Cut Impact on Small-Caps:

- Bullish Case: 1–3 cuts (0.25–0.75%) could lift Russell 2000 10–20% by 2026, with consumer durables (LCII, BC) and tech (NSIT) leading, per web data.

- Bearish Case: Fewer cuts (0–1) or tariff escalation could cap gains, with small-caps lagging SPY by 5–10%, per web data.

- Investment Approach:

- Buy: LCII, BC, WINA for value and discretionary spending exposure, targeting dips (e.g., LCII <$100), per web data.

- Hold: VRRM, NSIT for growth, monitoring tariff and recession risks, per web data.

- ETFs: iShares Russell 2000 ETF (IWM, 1.5% yield) for broad small-cap exposure, up 9% in July 2024, per web data.

- Portfolio Allocation:

- Allocate 5–10% to small-cap stocks, balancing consumer durables (LCII) and tech (NSIT), per prior analyses.

- Hedge with 3–5% in gold (GLD, +3%) or utilities (XLU, +1%) to counter tariff and recession risks, per prior analyses.

- Timing:

- Buy on SPY dips near $490–$500 or Russell 2000 pullbacks, per Trade That Swing.

- Dollar-cost average to manage VIX (~20–25), per Schwab.

- Key Catalysts to Monitor:

- July 9 Tariff Deadline: Reinstatement of 125% China tariffs could raise costs 10–20%, per web data.

- U.S.-China/EU Trade Talks: Resolutions could lift SPY 3–5%, easing small-cap pressures, per web data.

- June 17–18 FOMC Meeting: Rate cut signals (25 bps in September) will drive small-cap sentiment, per X post (@grok).

- Q2 Earnings (July): Small-cap earnings (42% growth) will clarify resilience, per web data.

- OBBBA Senate Progress: Deficit concerns could push yields to 4.5–5%, per web data.

- Consumer Spending: 13% retail cuts and 50.8 sentiment gauge small-cap demand, per prior analyses.

- Risks:

- Tariff Escalation: 125% China tariffs (July 9) could increase small-cap costs 10–20%, per J.P. Morgan.

- Recession Risk: 60% probability could curb demand, hitting small-caps harder, per web data.

- Fewer Rate Cuts: Only two cuts (0.5%) could limit small-cap upside, per web data.

- Inflation Surge: 4–4.5% inflation from tariffs could delay cuts, per web data.

- Valuation Pressure: Rising yields (4.5–5%) may depress small-cap P/Es, per web data.

- Rate Cut Impact on Small-Caps:

- Conclusion: Betting on the Fed’s Next Move:

- The Fed’s potential rate cuts in 2025, likely starting September with 1–3 reductions to 3.50–3.75%, could ignite small-cap stocks by lowering borrowing costs and boosting 42% earnings growth. However, Trump’s tariffs, deficit-driven yields, and a 60% recession risk threaten to cap gains, with small-caps (Russell 2000) lagging SPY (-19% vs. -15.6% YTD). Investors should target undervalued small-caps (LCII, BC) on dips, hedge with defensives, and monitor trade talks and Fed signals to seize opportunities in a volatile market.

- Why It Matters: With U.S. rates at 4.25–4.5% and the Fed poised for cuts, small-cap stocks stand at a crossroads in 2025’s $1.7 trillion market. Trump’s OBBBA tax cuts fuel spending, but tariffs and deficits cloud the outlook, with SPY down 15.6% YTD. Strategic buys (LCII, WINA) and diversified ETFs (IWM) offer a path to capitalize on a potential small-cap rally. At GLHR Investing, we’re here to guide you through the Fed’s next move, powering your portfolio in a high-stakes economy.

Invest smart with GLHR Investing—fuel your wealth with small-cap potential!

Disclaimer: GLHR Investing is not a financial adviser; please consult one.